M&A Risk in Review 2020-21 Part 2:

Risk and Mitigation

Welcome to Part 2 in Aon’s three-part 2020-21 M&A Risk in Review deep dive, a report conducted in partnership with Mergermarket. We look forward to the conversation around our findings. Please share this information with your networks.

Risks and Risk Mitigation

The risk landscape did not just shift in 2020, it was turned on its head. Naturally, the ongoing health crisis looms large in the minds of investors. However, putting the COVID-19 pandemic to one side, there are numerous other downside variables to consider that have the potential to impact upon dealmakers and the M&A targets they are seeking out.

Difficulty in accessing deal financing is the primary concern, cited by 38% of respondents as among the top two impediments standing in their way. The debt financing outlook has since shown signs of improvement, buoyed by the vaccination program. The vaccine roll-out is encouraging a return to some semblance of normal economic activity. This, in turn, has improved trading conditions and the ability of companies in more precarious sectors to repay their debts.

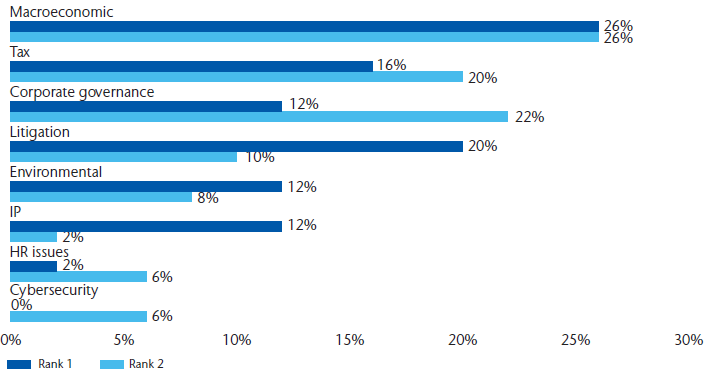

Apart from the ongoing COVID-19 crisis, what do you think will be the two greatest impediments/ sources of risk for dealmakers over the next 12 months? (Select top two and rank 1-2, where 1 is the greatest impediment and 2 the next greatest)

From the perspective of risks that impact deal targets specifically, 52% of respondents say macroeconomic factors are among the top two risks over the coming 12 months. While 2020 has drawn to a close with some welcome developments and forecasts point to a rebound this year, the International Monetary Fund predicting 5.2% growth, this is far from guaranteed.

What are the biggest risks you foresee at potential M&A targets over the coming 12 months? (Select top two and rank 1-2)

It is not only economic risk that concerns investors. More than a third (36%) of respondents cite tax as a one of two major risks affecting M&A targets. Once again, Biden taking office has implications here. One of the biggest changes made under Trump’s Tax Cuts and Jobs Act was the slashing of corporation tax from 35% to 21%. Under Biden’s proposed tax plan, the rate would be increased to the midway point of 28%, which would limit companies’ profitability.

Risk Adjustments

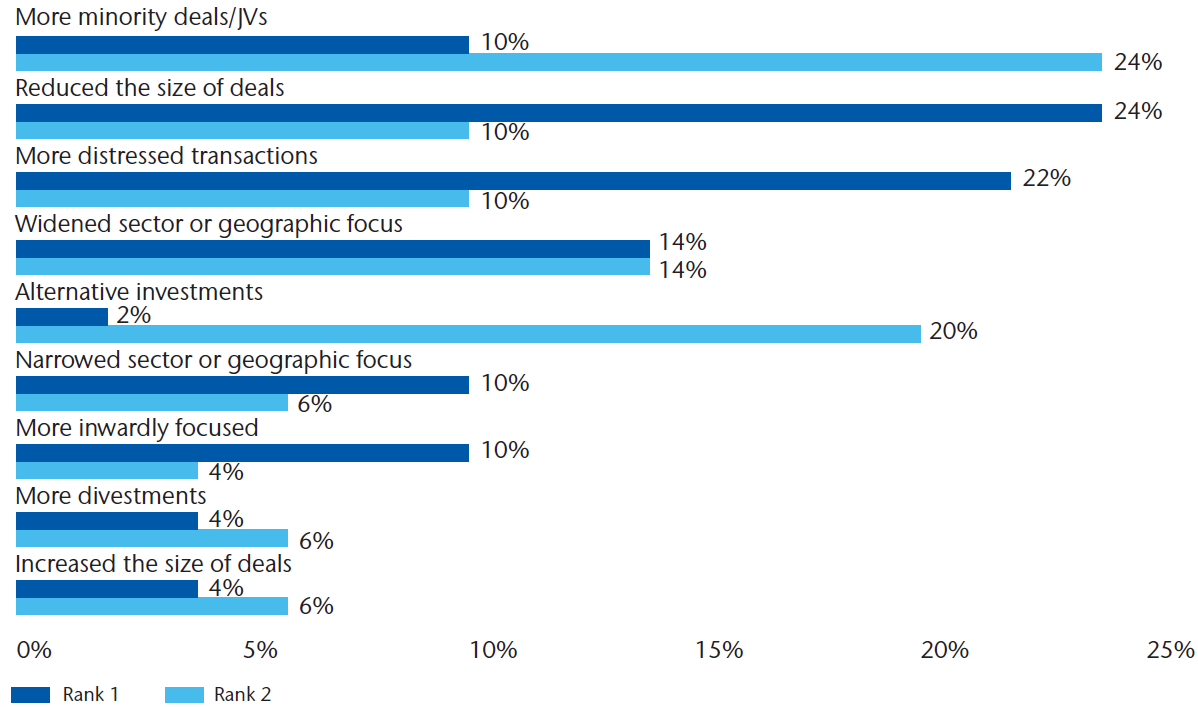

Given the heightened risk environment of 2020, investors have had to think smart and readjust their M&A strategies. This may include doubling down on a core strategic focus or simply sitting on the sidelines altogether until a clearer path forward emerges. The top risk mitigation strategies cited by respondents in our research, however, have been to participate in more minority deals and joint ventures (JVs) and reduce the size of their deals - both approaches cited by 34% of those surveyed.

What steps have you taken to change your M&A strategy since the start of 2020? (Select top two and rank 1-2)

Taking minority positions can increase risk if investors forgo certain powers, although this can be resolved with the inclusion of supermajority voting rights, preemptive rights, tag-along rights and other powers to protect their investment. At the same time, putting down a smaller equity outlay in a minority stake or simply a majority stake in a smaller company can help to minimize capital risk if the business does not perform as expected.

A similar proportion of investors (32%) also say they have adopted distressed strategies in 2020, which aligns with the deal environment. Government intervention to prop up economies through bond and loan buying programs has bought additional time for many companies. However, as these programs unwind, more distressed opportunities are likely to come to market.

Investors will be paying close attention to the performance of businesses and many will be taking pre-emptive action by proactively starting dialogue with these companies and their primary lenders, rather than waiting until the last minute for them to topple over.

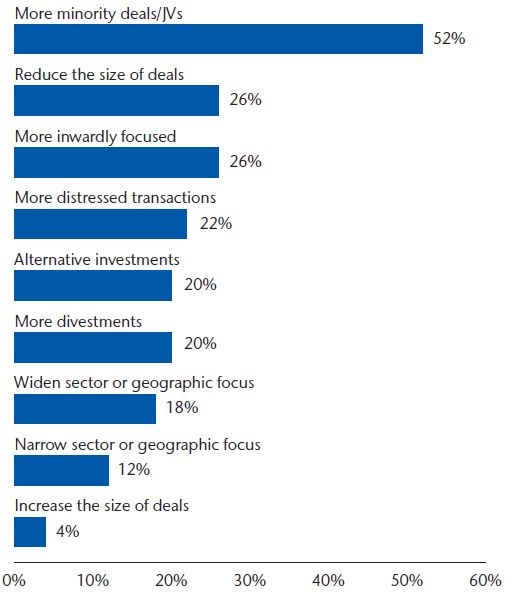

The risk mitigation strategy that most respondents foresee adopting in the future is pursuing more minority deals/JVs, 52% identifying this as one of their top two likely courses of action. There besides, respondents also cite reducing the size of deals (26%) and engaging in more inwardly focused activity (26%).

Due diligence – an even higher priority

Due diligence is a critical component of any deal. In times of economic stress and uncertainty, however, deeper, more rigorous diligence is often warranted to triple test assumptions and ensure the fundamentals of the target business are as advertised. An overwhelming majority (96%) of respondents say they are dedicating more resources to due diligence because of current economic conditions. Understanding the likely performance of a given sector or sub-sector is as important as determining the company’s performance within that space. The managing director of a Chinese PE firm says that balancing this outward-looking perspective with a thorough look at the business can help avoid legal issues. “Adequate due diligence preparation is essential to mitigate any litigation risk. Not just the target’s performance, but the external factors and geopolitical risks should also be measured appropriately.”

The COVID-19 pandemic has clearly made deal making more challenging, not least because negotiations have to be conducted remotely as people continue to avoid all but absolutely necessary travel. Technology has played a major role in helping acquirers understand the inner workings of target companies. Tools such as sophisticated virtual data rooms and the application of advanced data analytics have minimized disruption to M&A, allowing in depth, incisive due diligence and negotiations to be undertaken at arm’s length. “Use of new technology for assessing the risks is one practical way to mitigate them. Technology solutions complement the risk management principles of the organization and provide useful data to support decisions,” says the managing director of a UK investment bank.

Considering the current economic environment, are you dedicating more resources than in the past to due diligence processes when considering a transaction? (Select one)

What steps do you envisage taking in the future? (Select top two)

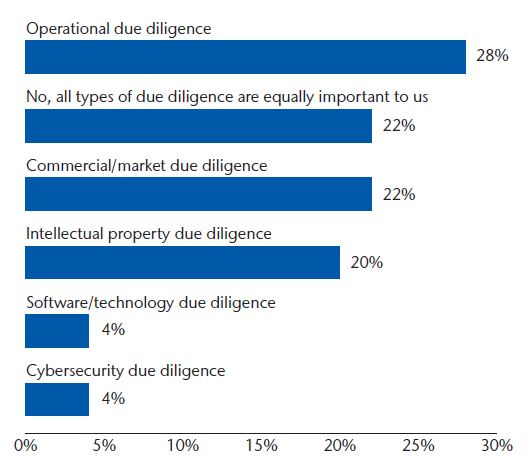

Diligence comes in various forms and our research indicates no one type takes absolute priority. For instance, we find that while 28% of investors are paying particularly close attention to operational due diligence, putting it ahead of all others, commercial/market due diligence (22%) and IP due diligence (20%) are not far behind. Meanwhile, 22% of respondents did not specify and say all types of due diligence are equally important to them.

Are you paying particularly close attention to any of the following types of due diligence? (Select one)

28% of investors are paying particularly close attention to operational due diligence, putting it ahead of all other types of due diligence

From our own work, we are seeing an increasing focus on IP diligence among clients. This involves assessing the integrity of claims to ownership of intellectual property critical to the success of the company that is up for sale. Buyers need comfort that a third party does not have a legitimate claim to the IP and that all disclosures about those assets have been made in good faith. Deeper audits may check the enforceability of patents and whether there is any history of litigation or undisclosed information that relate to patents on the IP.

COVID Credit Risk

The COVID-19 pandemic has unquestionably impacted companies’ credit risk. For one, businesses within sectors hit by the crisis, namely industries that rely on physical interaction and face-to-face working, have seen their revenues collapse in 2020 amid lockdown measures and the economic downturn. Weaker turnover and earnings in turn inhibit the ability of a company to repay its existing liabilities, increasing credit risk.

Another factor is market access. Sturdy credits in industries such as technology and non-discretionary retail, which have demonstrated extreme resilience to the effects of the pandemic, are highly sought after among lending institutions and bond investors and should not have trouble tapping markets to raise cash. This is especially true given that interest rates around the world have been cut back to or near zero, making investors hungry for yield.

However, highly exposed companies will have to pay high coupons in order to access debt, especially in high-risk periods if the pandemic continues to wax and wane. “Dealing with credit risk will be challenging because financing opportunities are also limited. To ensure that operations are functioning at par with expectations, capital investments are required. If this is not possible, it will affect goals,” says the managing director of an investment bank in Canada.

The unpredictable nature of the pandemic and its downstream effects on companies and their suppliers also make credit risk open to a greater degree of interpretation, says the managing director of an investment bank in Australia. “Terms of the agreement and warranty discussions are taking longer to formulate. Credit risk will also depend on perception, as we see in the case of varied opinions during valuation discussions between buyers and sellers.”

The speed and severity with which the pandemic has buffeted companies has only increased the subjectivity of credit risk calculations, an observation made by numerous respondents in our research. For instance, the group director of M&A at a French corporate says that “because Covid-19 has been a massive shock to operations, relying on the company’s most recent financial data is of limited help in judging credit risk”. Meanwhile, a partner at a US private equity firm tells us that “it is vital to evaluate the external climate and its effects on the target, without discounting the company’s actual potential”.

An Overview of the M&A Risk in Review Report

In our latest Risk in Review report, in partnership with Mergermarket, we explore investors’ M&A expectations for the next 12 months, the sectors they believe will outperform expectations, the strategies employed to mitigate key risks beyond COVID-19 and how and why the suite of available M&A insurance products are being used, among other areas. This report is based upon surveys of senior executives from corporate development teams, private equity firms and investment banks.

Looking Forward

We hope you have found this first part in the M&A Risk in Review 2020-21 series insightful and that it will continue to spark conversation. We look forward to hearing your thoughts and feedback and stay tuned for Part 3 of the report highlights.

About Aon

Aon plc (NYSE:AON) is a leading global professional services firm providing a broad range of risk, retirement and health solutions. Our 50,000 colleagues in 120 countries empower results for clients by using proprietary data and analytics to deliver insights that reduce volatility and improve performance.

© Aon plc 2021. All rights reserved.

The information contained herein and the statements expressed are of a general nature and are not intended to address the circumstances of any particular individual or entity. although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

All descriptions, summaries or highlights of coverage are for general informational purposes only and do not amend, alter or modify the actual terms or conditions of any insurance policy. Coverage is governed only by the terms and conditions of the relevant policy.

Subject to availability in applicable state